What Ghost Kitchens Got Wrong

Two good ideas and one bad mistake

Changing Lanes covers innovative mobility in all its forms. One of our interests is the economics and politics of how cities move: transit, freight, urban logistics, and the platforms reshaping them. This piece is the second in an informal series on platform power in the economics of city life; the first, on Uber, ran earlier this year.

In 2020, Wendy’s and REEF Technology announced they would build 700 delivery kitchen locations across North America. These would not be restaurants, but just kitchens, sited in parking lots and operated entirely for delivery. It was a confident bet about a new way fast-food brands could make money. Not with dining rooms, drive-throughs, and a real-estate premium, but with just the food, dispatched to wherever the customer happened to be.

Less than two years later, Wendy’s CEO told investors the company no longer saw delivery kitchens as part of its growth trajectory. The target, which had already fallen from 700 to 150, fell to zero. Why the pivot? Because average annual revenues at REEF locations had come in below $500,000, or less than a third of what a typical Wendy’s restaurant generates. The REEF locations disappeared, and the parking lots went back to storing cars.

Ghost kitchens, commercial kitchens with no dine-in option that prepare food solely for delivery, were supposed to transform urban food service. A recent edition of Brian Potter’s Construction Physics newsletter, “Is the Future ‘AWS for Everything’?”, is worth reading for its main argument about economies of scale; right at the end, he uses ghost kitchens as a quick illustration of how those economies don’t always pan out, then moves on. Potter’s piece reminded me that five years ago, I was quite bullish on ghost kitchens as the future, before I set the matter aside to think about other things. Looking into it, I was surprised to learn that my analysis back then was dead wrong.

The evidence shows that ghost kitchens have indeed failed. But the emerging narrative about why—pandemic buzz around food delivery, venture capital poured in, post-pandemic consumers returned to restaurants, concept collapsed—is a poor explanation.

Here’s a better account. The ghost kitchen concept bundled two distinct, legitimate claims—a real estate thesis about urban land arbitrage and a mobility thesis about the structural shift to off-premises dining—and both were borne out. But there was a third, hidden claim about who would capture the value generated by those kitchens, and that assumption proved spectacularly false.

Two Good Ideas…

Ghost kitchens were delivering on two claims at once.

The real estate thesis said: urban land near residential density has value that traditional restaurants aren’t capturing.

At minimum, a good foodservice operation of any kind requires quality ingredients and a capable kitchen, by which I mean not only the physical capital of stoves and ovens, but also the human capital to use it.

A traditional restaurant needs these, but also much more. It needs a ‘front of house’: hosts, servers, and others who deal with customers. It needs premises functional enough to serve patrons and attractive enough to make them comfortable: not only tables, chairs, cutlery, and so forth, but square footage to feature them all. It needs to be reachable, meaning it needs adequate parking, decent transit access, or both. It needs to be in a part of the city that patrons will find to be safe and appealing. And it needs to be close enough to where people live and work that the trip doesn’t feel onerous. Taken together, these requirements mean that the restaurant must be itself, and be in a place, that is desirable, accessible, and visible.

That combination costs money. The rent or mortgage a restaurant must be able to cover imposes a floor on the revenue it needs to generate.

The appeal of a ghost kitchen was that it could shed most of this. Forgoing front-of-house staff would cut operational costs, but more importantly, it would cut capital costs. It could do that in two ways: not only would the ghost kitchen not need to devote space to customer areas, it wouldn’t need to site itself on expensive land at all. It could locate itself in an unappealing part of the city, where land was cheap; even, at the smallest scale, in a retrofitted shipping container in a low-volume parking garage.

But that didn’t mean it could set itself up anywhere. Instead of needing to be somewhere customers would be willing to travel, it would need to be close enough to where enough customers lived that their meals could arrive in a timely fashion, and where delivery costs wouldn’t break the value proposition. Last-mile delivery cost and speed depend heavily on proximity to the people being served, a mechanism that readers of Changing Lanes will recognize also applies to transit and freight.

That was the real estate thesis: that there was enough commercial land unsuitable for a traditional restaurant, but near enough to dense clusters of people, to support this new business model… and that the market hadn’t yet priced this value in, meaning there would be arbitrage opportunities by moving quickly.

The mobility thesis said: restaurants built around sit-down service are poorly designed to also offer delivery service.

This claim follows from how restaurants are built. Their layouts are organized around the dining room: the kitchen is sized to feed the tables, not to maximize throughput. Their equipment and workflows are all calibrated for food that travels ten metres to a table, not ten minutes in an insulated bag. Their ingress points are not optimized for courier access; their front entrances are easy to reach, but courier vehicles would then be taking up space for patrons, and patrons don’t like it when delivery trade is happening in their space. Couriers might instead use back entrances and not disturb patrons, but those areas are deliberately hard to reach, and often can’t be accessed quickly, which delivery couriers require.

This awkwardness supposedly gave ghost kitchens an edge. For the delivery market, a purpose-built production kitchen, designed from the start around delivery—optimized for throughput, packaging, and dispatch rather than ambience and table turns—would in theory outperform a retrofitted dine-in operation on every dimension that mattered.

All of this is true a priori, but was meaningless until quite recently, because food delivery was a niche business. Younger people may not believe it, but well into living memory, the only food one could readily order and have delivered to one’s door was pizza (and, in some markets, Chinese food). The advent of the mobile Internet changed this by making delivery platforms feasible. Once it was possible to order food from one’s couch via a phone's interface, DoorDash, Uber Eats, and SkipTheDishes emerged to aggregate demand and handle logistics. Before the pandemic, meal delivery was already becoming a broadly accepted substitute for going out, but Covid accelerated the trend by making it the only option: dining rooms closed, people stayed home, and delivery volume spiked.

The arrival of food delivery as a business sector made the gap between an existing restaurant's ability to serve delivery markets and a kitchen designed for that purpose apparent for the first time. That was the mobility thesis: that custom-built kitchens for the delivery market could outperform traditional restaurants in that market, and that there was a first-mover advantage to siting and building those kitchens where they could offer the most value.

These were different bets, about real estate and about the food-service market, but proponents bundled them into a single proposition: a commercial kitchen without a dining room. What connected them was a shared assumption that whoever controlled the production infrastructure would capture the value it generated.

That assumption, it turned out, was the load-bearing one.

…and One Bad Mistake

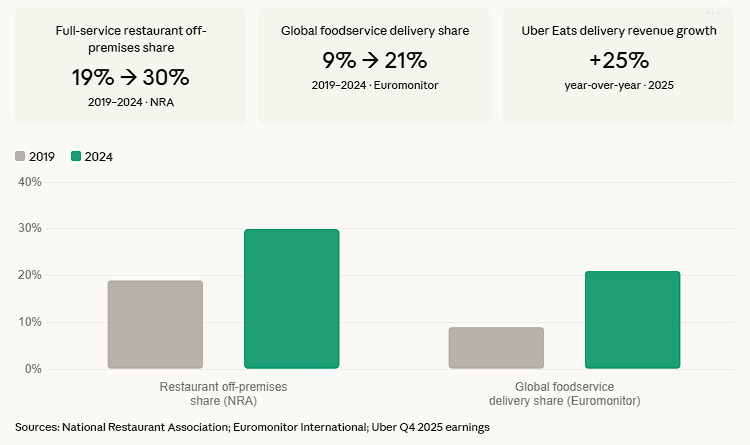

Before turning to where the analysis broke down, it’s worth being precise about what didn’t. Both underlying theses have proven valid.

Off-premises dining is not a pandemic blip that reverted when lockdowns ended. The demand that ghost kitchens were built to serve is real, growing, and profitable.

Data visualization courtesy of Claude, sourced from NRA, Euromonitor, and Uber

The centralized production logic is also sound, in contexts that match its requirements. Reports say that of kitchens serving caterers, meal prep businesses, packaged goods producers, and institutional clients, two-fifths are making a profit and another two-fifths are breaking even. Meanwhile, hospital and institutional food service has adopted centralized production, with meaningful budget savings. These aren’t ghost kitchens as anyone in venture capital imagined them, but they vindicate the underlying logic: high-volume, repetitive, centralized production serving known customers through predictable channels works.

So ghost kitchens had every opportunity to generate business. Unfortunately, what they didn’t have was an opportunity to make a profit on that business. The shared assumption—that controlling the production infrastructure meant capturing the value it generated—failed, and it failed on both theses separately.

The mobility thesis broke on the customer relationship. A purpose-built delivery kitchen, however superior on every production dimension, owns the production but does not thereby own the customer. That’s true for two reasons.

The first is trust. The National Restaurant Association found that 70% of consumers say it matters to them that their food comes from a restaurant with a physically-accessible location. Customers who discovered they had ordered from a major chain operating under a made-up virtual brand name—who had been, as they put it, “catfished”—were upset because they had been deceived about something they cared about, and insisted that such places had to explicitly disclose that that was what they were.

One reading of this preference is that people want the dining experience: the room, the occasion, the presence of other people eating around them. On this reading, takeout is a substitute for dining in, and a delivery partner that has no such option is no substitute at all.

That reading isn’t wrong, but it’s incomplete. We might imagine customers don’t want to order from ‘No-Name Burger Bar’, which lacks brand value or associations with an in-house dining experience; but they should, on this view, be perfectly happy to order from a ghost McDonald’s or ghost Burger King. The whole point of big burger chains like these is that their food is a commodity, prepared the same everywhere, and they have deep and broad brand association and value, meaning that such a facility should not face any trust problem at all.

And yet Wendy’s, whose collapse from 700 REEF locations I wrote about at the beginning of this piece, is the clearest illustration that this reading isn’t enough. Less than two years after the original deal, the unit economics had simply never materialized.

A Wendy’s ghost kitchen, image courtesy of of this Wendy’s press release from 2021

Why? The answer appears to be that consumers are being practical. They want accountability, someone to hold responsible when things go wrong. And as far as customers are concerned, a dine-in restaurant that one can visit has (or seems to have) feedback loops that will make the operators care about hygiene and food safety in ways that an anonymous industrial kitchen will not.

Whether or not this is rational, this is how customers seem to think, and the customer is always right.

The second reason was lack of customer loyalty. A restaurant with a physical presence earns returning customers passively: a good experience encourages repeat business. A virtual brand is not so fortunate, because it doesn’t sell experiences, just food as a commodity. Every customer therefore is a new prize to be won, from the beginning, every time, through a platform that charges for the privilege and has no stake in whether any particular brand survives. 41 of 71 restaurants across five CloudKitchens locations had closed within one year; a 58% annual failure rate, because customer acquisition was a permanent operating cost, not a compounding investment.

Lack of trust or loyalty are two faces of the same coin, namely that ghost kitchens have no independent relationship with their customers. The platform owned that relationship entirely.

So the mobility thesis did not hold. How about the real estate thesis?

Unfortunately, it broke too, and on a single, decisive point. The real estate thesis, you’ll recall, was that operating kitchens rather than restaurants, and on low-value land, would create a significant margin relative to incumbent food producers, and the ghost kitchens would capture that margin.

They reckoned without the delivery platforms. The platforms wanted that margin, and the ghost kitchens couldn’t stop them from taking it.

A restaurant using a delivery platform pays a commission on every order, and often additional fees for marketing placement and payment processing as well. At the time the ghost-kitchen investment cycle was spinning up, the pandemic had made food-delivery the only game in town for meals outside the home, and so multiple U.S. cities moved to cap them at around 30% of the order price. It was against that backdrop that ghost-kitchen investments were made, assuming those rates as a baseline.

Unfortunately low rates were an artifact of the pandemic, and began to rise as Covid receded. While some cities, like San Francisco and New York, attempted to make their caps permanent in 2021, the platforms pushed back in court, and by 2023, they had largely won. New York held out longest, but as of April 2025, even that city had compromised. The new framework there allows 15% for core delivery, 5% for basic marketing visibility, and 3% for payment processing, plus an “optional” enhanced services tier of an additional 20%, covering expanded delivery radius and promotional placement, for a potential total of 43%.

(And 43% is not really optional; operators who decline the enhanced tier are deprioritized in platform search rankings, meaning that the real choice is between paying 43% or being buried algorithmically.)

Certainly a conventional restaurant using a delivery platform pays a commission too, but this was not an existential risk for those businesses, since they only pay it on the portion of revenue that comes from delivery. For most full-service operators, that’s a minority of income. Most comes through the dining room, which the platform never touches. Since a ghost kitchen has no dining room, the commission that is manageable for a restaurant with tables is lethal for an operator without them.

In any case, the failures of the mobility and real-estate theses reduce to the same point, which is that they both assumed if the food producer could generate value, they could keep it. But that was wrong: in the delivery economy, the platform can seize that value, and will.

The Platform Takes the Margin

What remains is an opportunity that hasn’t materialized, and seems unlikely to, even though the two theses about their value are still true. Parking lots are still underused, dead retail is still everywhere, and cities still contain spaces that sit between the density that creates demand and the production infrastructure that could serve it. And it will always be the case that a restaurant optimized for serving in-house customers will find it difficult to serve the delivery market.

Given that, what would need to change for ghost kitchens as originally conceived to succeed? In my view, one of two things.

One would be a substantial fall in delivery platform commission rates. That seems unlikely, given the direction of the NYC settlement and the platforms’ demonstrated willingness to litigate caps into the ground.

The other would be operators building direct-to-consumer channels that bypass platforms entirely. That seems equally unlikely: it requires exactly the kind of marketing investment and customer-acquisition infrastructure that the ghost kitchen model was designed to shed.

I think the old analysis is still correct; urban land near residential density has logistics value that is currently underused. But it was an error to assume that the value created by unlocking that land would accrue to the one who did the unlocking. It accrued, instead, to the one who controls access to the customer. In the delivery economy, that’s the platform.

This is a pattern that Changing Lanes has traced before. In January, writing about Uber, I argued that what Uber’s subsidy years bought wasn’t network effects, but market power. By the time Uber started charging riders more and paying drivers less, there was no competitor left to undercut it and no regulator with the will to stop it.

Ghost kitchens have been losing the same race. The delivery platforms that ghost kitchens depended on had spent years, and billions, acquiring the same kind of structural dominance. When ghost-kitchen operators tried to capture the margin their model had created, the platforms were already there, and better armed: with commission structures, algorithmic levers, and litigation budgets against regulators.

The question of who captures the surplus generated by urban-logistics infrastructure is the key question of platform urbanism. Ridehail and ghost kitchens are a case study in the answer to that question. The answer, so far, seems to be that the platform always wins.

Respect to Jannik Reigl for feedback on earlier drafts.

It is scary how we often seem to cover the same turf. Six years ago, I worried about Reef and ghost kitchens, saying that in the future, "We will all be poor, fat, and buried in plastic." I am relieved to find that they didn't work out. https://www.treehugger.com/future-food-imaginary-brands-cooked-ghost-kitchens-4857104