Canada's High-Speed Rail Is the New Seaway

Canadian megaprojects that miss the boat

This is the fourth piece in my ongoing series on Alto, Canada’s proposed high-speed rail project. Earlier pieces argued that the project has the wrong structure, depends on a regional rail network that doesn’t exist, and is making poor choices about where to put its stations. This piece makes a different argument: that Alto is not being wise in its forecasts.

Before we get to that, though, two reminders:

Firstly: this Thursday, 28 May at 1200h EST, you are invited to attend the first Changing Lanes livestream! My first guest will be Bern Grush, a co-author of my book The End of Driving, on the future of urban mobility, and the start-up he’s founded to build that future. Fair warning: Bern and I have some disagreements on this subject, which we will probe. I think it will be a fun conversation! Subscribers will be notified when we go live, but you may also sign up here.

Secondly: a reminder that in three weeks—specifically, Tuesday, 16 June—the price of a subscription will go up. The current rate of US$10/month or US$100/year ends; from that date, new subscriptions will be US$13/month or US$130/year. Existing annual subscribers keep their current rate until renewal, while monthly subscribers move to the new rate on the first billing cycle after 16 June. What that means is, if you’ve been thinking about subscribing, now’s the time, since annual subscriptions taken at today’s rate will be locked in for a full year.

Alto, Canada’s putative high-speed rail (HSR) project, has a published business case. It also has consultation FAQs (which cover 50 topics, including winter resilience and Indigenous collaboration), a Transport Canada environmental and economic assessment, and published testimony from its CEO to the Senate of Canada.

Nowhere in any of these documents is any treatment of automated vehicles (AVs) as a demand risk to the project. There is no spirited engagement with AVs; nor a hedged acknowledgment of them; not even a dismissal. There is no treatment of AVs at all.

That’s remarkable, because Alto is an infrastructure project, projected to cost $60–$90 billion CAD. Bear in mind that driverless freeway service and driverless intercity trucking are both already in commercial operation, meaning that it’s reasonable to expect highway-and-urban AV, privately owned and/or available for hire, by 2035, before Alto’s first segment is scheduled to carry a fare-paying passenger.

In other words, Canada seems poised to build a massive infrastructure project through the heart of Quebec and Ontario, at massive cost, even though its value proposition may be superseded before the first train runs.

It has happened before. Consider the St. Lawrence Seaway.

The Seaway opened in 1959, a joint Canadian and American project that gave ocean-going vessels the ability to travel 3,700 kilometres inland, as far as Duluth and Thunder Bay. It was one of the great engineering achievements of the postwar era.

That may sound like success. It is, but unfortunately a heavily qualified one. The Seaway reached its peak in 1977, and today carries two-thirds of the cargo it did then, fifty years ago. It ships bulk commodities, mostly grain and ore, and essentially no container traffic.

Alto is on course to become the Seaway of our era: a project that construes a problem, and solves it at immense cost, even as the world changes such that the problem recedes in importance. Canada’s embrace of it suggests that, once again, the country will skate to where the puck has been and ignore where it is going.

Why the Seaway Underperformed

The St. Lawrence Seaway was a genuine achievement.

Grlakes lawrence map-blank.svg, CC BY-SA 4.0, via Wikimedia Commons

{kind=link}

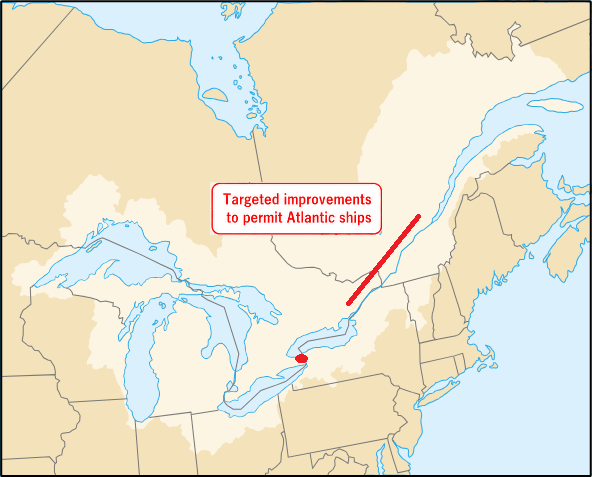

The problem it was trying to solve is immediately evident upon consultation of a map. The St. Lawrence River drains the vast inland seas of the Great Lakes. The St. Lawrence narrows beyond Montreal, which was not an accident; Montreal grew up where it did precisely because that was as far as ocean-going vessels of the pre-industrial age could reach. But after 300km of intermittently tight and sloped stretches, the river widens out into Lake Ontario. It was clear from Canada’s early days that the construction of locks along the Montreal-to-Kingston segment could permit Atlantic vessels to reach Toronto; further upgrades to the Welland Canal would grant access to Detroit; and further work beyond would open up the remainder of the Great Lakes, bringing ships as far inland as Chicago, Thunder Bay, and Duluth.

Canada had urged construction since the early 1900s, but opposition from American railways and ports blocked it for decades (they didn’t want competition). The deadlock broke in the early 1950s, when post-war anxieties about iron-ore supply for the U.S. steel industry gave the project the national-security framing it needed. Enabling legislation passed in 1954; construction took just under five years, with the formal opening in June 1959. It cost about $460 million CAD, with the Canadian government paying slightly more than two-thirds; Canada spent a further $300 million enlarging the Welland Canal. The Seaway came in on time, within authorized budgets, and has been continuously operational for sixty-five years and counting.

The Seaway was a success, at first. Cargo volumes rose through the 1960s to peak at just over 57 million tonnes in 1977. Since then, it’s been in slow decline: today the Seaway moves roughly 37 million tonnes, of which three-quarters is still iron ore and grain (almost no consumer goods).1

What happened? Why did the Seaway become only a modest success?

In a word: containerization.

The containerization revolution is well known. By shipping goods of all sorts in a standard container (eight feet wide, eight and a half tall, twenty or forty long) that could be moved en bloc from ship to railcar to warehouse, the costs—in transshipment, in security, in protection—of goods movement dropped, enabling the globalized economy we enjoy today. Containerization kicked off when the converted T-2 tanker, the Ideal-X, carried 58 thirty-five-foot containers from Newark to Houston in April 1956. Within fifteen years, the container had remade global shipping, a revolution the Seaway missed entirely; today it moves virtually no containers.

Why? For two reasons.

The first is structural. The Seaway’s locks are sized to match the existing locks on the Welland Canal. Containerization encouraged the emergence of bigger ships with deeper drafts, rated Suezmax or Panamax (the maximum size that could be accommodated by the Suez and Panama Canals). The Welland is too small, limiting competition and capacity.

But so what? Why didn’t smaller container vessels, sized to fit the Welland locks, emerge? That was because of the second reason: economics. Bulk cargo like the Seaway was built to handle, grain, ore, and coal, tolerates slow, seasonal, low-cost transit because the goods are low-value-per-tonne and inventory carrying costs are low. A shipload of iron ore can sit in transit for weeks without straining anyone’s balance sheet. But containers are not like that. Containerization collapsed the time and labour cost of port-to-port transfer. Removal of that bottleneck changed the game, creating a new market: carriage of high-value goods on tight delivery schedules in supply chains designed around just-in-time inventory. Bulk cargo shipping continued to compete on cost over distance, but containerization introduced a new higher-value market competing on speed.

The Seaway was built for the former, not the latter; shipping by the Seaway was and is slow. The full Seaway run from Duluth to Montreal runs five to seven days, with the Welland Canal alone taking roughly twelve hours to transit. Compare that to travel time from the Port of New York and New Jersey, the ‘must-call’ container hub for the U.S. Northeast. From there, a truck can reach most of the Great Lakes industrial heartland, i.e. the Seaway’s terminal point, inside twenty-four hours. (Rail can do it within forty-eight.) The Seaway’s structural disadvantage on container time-to-market is roughly an order of magnitude.2

In the decades since containerization came to dominate global shipping, the Great Lakes ports have tried to adapt the Seaway to the new world, but in vain. Sea3, sponsored by the Hamilton Port Authority, began container feeder service to Montreal and Toronto in July 2009 and was terminated within roughly a year. The Great Lakes Feeder Line began service from Halifax to Montreal and Great Lakes interior ports in July 2008 and lasted about as long. It’s notable those were both Canadian operators, eager to find alternative routes to market; no U.S. operator has attempted a Seaway container feeder service at all.

This was, and is, the Seaway’s problem: it is infrastructure built well for a paradigm that was already fading at the moment of construction. The Seaway asked “how do we move bulk cargo from inland to the sea?” just as a new question, “how do we connect North American industry to global container trade?” was about to emerge. The Seaway is a good answer to the first and no answer to the second.

Canadian Transfer, Niels Johannes, CC BY-SA 4.0, via Wikimedia Commons

{kind=link}

And yet, I come to praise the Seaway, not to bury it. An informed observer in 1954 would not have encountered any mention of commercial container service in trade-press summaries of cargo handling. The Ideal-X did not sail until 26 April 1956, almost two years after the Seaway’s inception. The first cellular ships (i.e., purpose-built to accommodate stackable containers) were not constructed until 1968. Canada’s first container terminal opened in Halifax in 1971, twelve years after the Seaway did. In 1954, the question “will containerization replace bulk handling?” had never been asked.

Which prompts us to wonder, has Alto missed anything important about the future movement of people?

It certainly seems that it has.

Why Alto Will Underperform

Stipulate that Alto succeeds if, once in operation, its fares exceed its operating costs; we will set aside its high-eleven-figure capital cost. We’re being generous in so doing, since any reasonable cost-benefit test would not set capital costs aside; indeed the project’s own business case does not. But it gives us a reasonable definition of ‘failure’, under which the AV question is fair game: a paradigm shift that suppresses ridership is a direct threat to the operating-revenue line. This is not a stringent test. The Tokaido Shinkansen passes it; so does Paris–Lyon. Where high-speed rail is well sited, fares cover operations and then some.

Today, in 2026, Waymo runs commercial driverless freeway service across Phoenix, San Francisco, Los Angeles, and Austin. Aurora has been running fully driverless freight trucks between Dallas and Houston, a corridor roughly the length of Alto’s first segment, since April 2025, with a second corridor (Fort Worth to El Paso, six hundred miles) added in Q3. The trajectory is unambiguous: driving automation is moving from urban geofences onto highways and from fleet to private-sale offerings. But Alto’s planners have not factored it into their plans.

So let’s do it for them, and consider: what are the likely consequences of automated driving, capable of both urban and highway travel, available at scale?

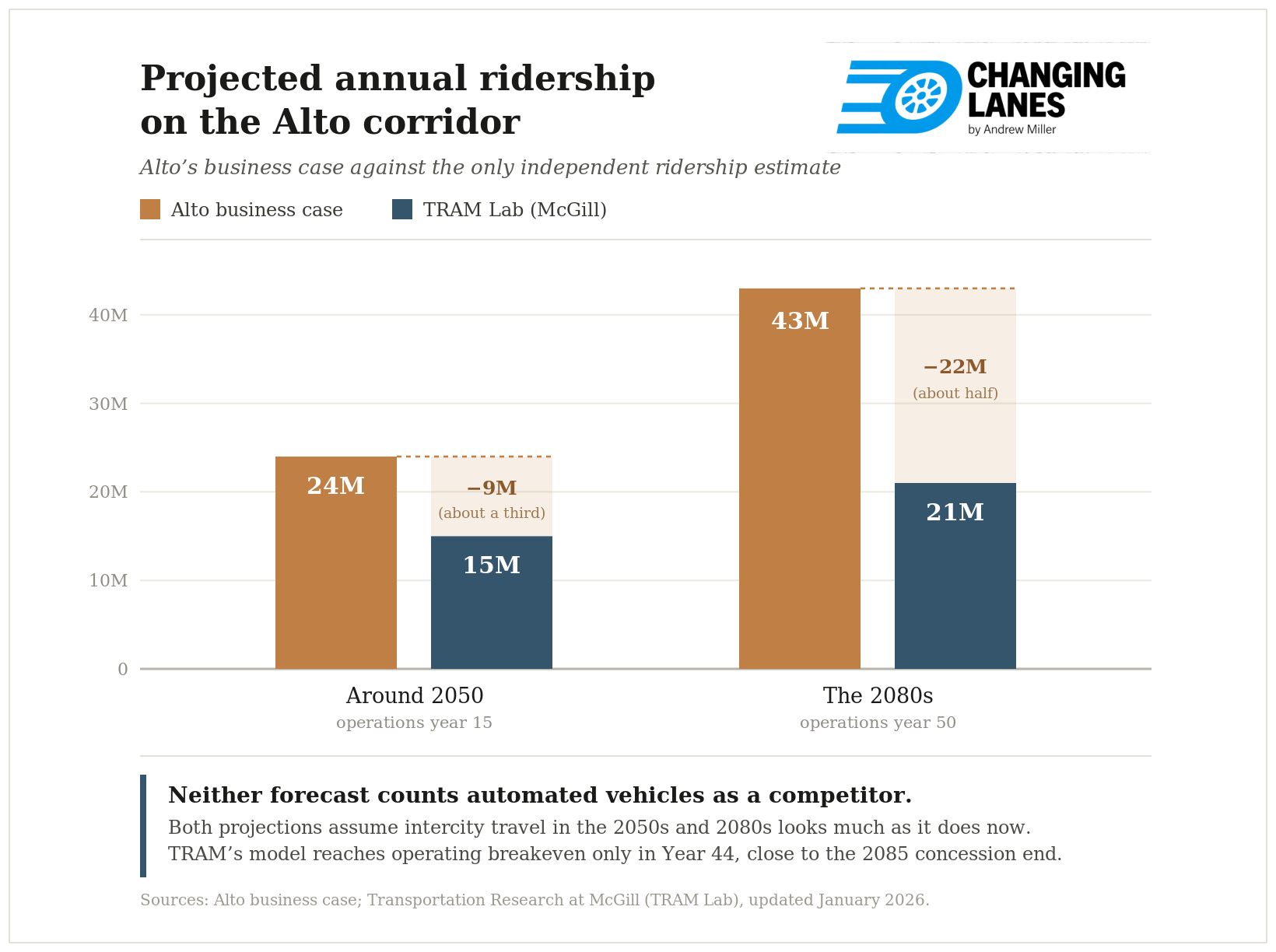

Alto’s business case projects 24 million annual trips by the 2050s, rising to 43 million by the 2080s. Those numbers assume intercity travel demand in the 2040s and beyond will look roughly as it does now: trips between fixed downtown nodes, on schedules, by people choosing rail over driving or flying. We only have one independent stated-preference study of demand on Alto’s corridor, courtesy of McGill University’s TRAM Lab. It reaches the much lower figure of ~16 million riders at Year 15 of operation, rising to 22 million by Year 50. The TRAM survey of 6,738 corridor residents found that one in three would take HSR at least once a year. Lead author Ahmed El-Geneidy has called even this estimate generous: “We gave them the benefit of the doubt [that] the demand is going to be really, really increasing very much.”

The TRAM analysis is bottom-up, built from stated preference, where Alto’s is top-down, built from a modal-share assumption that rail’s share of Toronto-Montreal trips will quadruple from 10 per cent to 40 per cent. Top-down HSR modal-share forecasts have a documented optimism bias; Bent Flyvbjerg’s survey of 210 projects in fourteen countries found that ridership forecasts systematically exceed delivered ridership.

So there is a problem: TRAM runs well below Alto at both horizons—about 15 million against Alto’s 24 million around 2050, and 21 million against 43 million by the 2080s—a shortfall that widens from a third to roughly half as the forecast runs out. Even before any AV consideration enters the picture, Alto’s investment case is teetering. And then driving automation (which, importantly, is not a factor in TRAM’s analysis either) gives the pillar another blow.

Specific predictions about the future of driving automation are a fool’s errand: there are too many unknowns to say what technology and services will exist decades from now. So let’s confine ourselves to general predictions, and imagine that there will be vehicles that can complete a roughly four-hundred-kilometre trip, without a human driver, on highways and metropolitan roads, and available for hire or purchase.

We can see such an outcome emerging, on two different trajectories. The robotaxi geofence keeps expanding: Waymo’s San Francisco service area, which started in part of the city’s eastern half, now covers roughly 260 square miles including SFO and the freeways into it. Robotaxi service starts in the dense urban core and steadily expands outward, picking up highway segments along the way. In parallel, privately-owned AVs are arriving: Tesla aims to sell vehicles without steering wheels to private buyers, and other manufacturers are developing comparable offerings. Either of these on its own delivers a viable intercity competitor; both happening at once is a likelier outcome than the planning case assumes.

That competitor won’t win on speed, but speed has never been the only axis that mattered. As I have noted before, HSR itself doesn’t win on speed; “high-speed” compares to other rail, not to commercial air, which wins by a wide margin. In its markets, HSR thrives anyway, because air’s terminal-to-terminal advantage is partly absorbed by airports being twenty to forty kilometres outside city centres, security screening adding half an hour, and baggage adding more. So against commercial air, HSR loses on speed but wins on overall trip time… if downtown is where the passenger is going. Similarly, AVs lose to HSR on speed but win on access, at trip end and beginning, since they are door-to-door and on no schedule.

Recall that the Seaway lost, even though it continued to beat container shipping on cost-per-tonne, because the relevant axis of competition shifted to speed-at-hubs. Similarly, an intercity AV (whether owned or hired) shifts competition from speed to convenience: AV solves the list of frustrations a rail or air traveller is asked to tolerate. These include getting to the station, getting from the station, travelling on a schedule, carrying luggage, sharing space with strangers, going through airport security (if flying), and on and on. None of those costs are large in isolation, but together they make foregoing them attractive.

An AV will incur none of these costs. It arrives where the passenger is and leaves them where they want to go. It runs on the road network that already exists and serves every destination in the country. As such it’s attractive for the very large share of trips that neither begin nor end in the downtown core, but somewhere in the metropolitan sprawl around it. For the rail passenger whose origin and destination happen to be downtown, the rail terminal is a convenience. For everyone else, it is the first inconvenience of the trip.

Will everyone take this option? Certainly not; a trip from Toronto to Montreal by Alto will take two to three hours less than by AV, meaning that rail wins on trips that require speed (but air will continue to beat rail on that metric). Similarly, the AV trip won’t be cheap. Long intercity trips are the hardest use case for shared-fleet economics: a four-hundred-kilometre haul ties up the vehicle for hours, and may require a deadhead return, which is the hardest pill to swallow. (Private vehicles dodge the deadhead cost, but only for those who own one.) But the question is not whether everyone will take this option, but whether enough will to imperil Alto’s business case. Business-class airfares run four to six times coach, and the cabins fill up; people pay for what they value, and what they value at the long end of the travel-comfort spectrum is freedom from terminals, schedules, queues, and other passengers. AVs offer a kind of intercity convenience that no rail product can.

Let’s make a defensible estimate for mass-market intercity AV capability — that is, a commercially-available vehicle that can complete a 400-kilometre highway trip without a human driver: let’s say it arrives by 2040. That is roughly the time we might expect Alto’s first phase to open, with the Ottawa–Montreal segment expected to carry fare-paying passengers in the late 2030s at the earliest. The full Toronto–Quebec City corridor has no published completion date, and Alto’s own FAQ says each construction phase takes seven to ten years.

I can’t say that AVs will absorb Alto’s ridership; predictions are hard. But I can say that Alto’s published case does not address this question at all. California’s HSR project has its share of failures, but at least mentioned AVs and ride-hailing in its 2018 business plan. Alto, authorized in 2025–2026, with Waymo on the freeway, does not.

What Alto Owes Us

The “Seaway question” survives the optimistic scenario for Alto: even if the project appoints excellent leadership, picks the right stations, reforms its process, and reaches its own ridership projections, the question remains. Was this the right problem to solve at this scale, with this technology on the horizon, at this moment?

I am dubious. I cannot prove Alto will fail; nobody can prove a project will fail 30 years before it opens. But I can say that Alto has not done the work to prove it won’t. A country committing somewhere between $60 and $90 billion to fixed-corridor infrastructure should be able to explain why distributed AI-driven mobility doesn’t make its bet obsolete before the first train runs.

I would love to see an Alto business case that explicitly stress-tests ridership against a 2040 Level 4 highway scenario. If the case holds even with aggressive AV adoption assumptions, my objections here lose their force. I hope that Alto’s planners engage this question seriously, and prove that I’m wrong. Until they do, here is the bet I’ll make. At TRAM Lab’s 15-million-rider scenario—itself two-thirds of Alto’s headline number—TRAM models a $1.28-billion annual operating subsidy, with the system not turning operationally profitable until Year 44. A meaningful AV haircut on TRAM’s already-conservative figure takes operating breakeven out of reach within the concession horizon. That is the specific risk Alto’s planners owe their public a serious treatment of. Until they provide one, I expect Alto to need indefinite operating support — exactly the structural pattern the Seaway settled into when Parliament wrote off its capital debt in 1977.

The Seaway opened in 1959 and almost immediately found itself in the wrong shipping era. Alto will break ground in 2029. The chance to ask whether it is being built for the right travel era is now, before paper is turned into cement.

Respect to Jeff Fong for comments on an earlier draft of this piece.

1977 was also the year Parliament passed legislation converting the Seaway Authority’s debt to equity. The move was a formal acknowledgment that the Seaway’s toll revenue would never repay the capital invested to build it… a matter to bear in mind when thinking about Alto.

And that’s during summer months: during the winter, the Seaway freezes and becomes impassable. In the 1950s, when the Seaway was being planned, the status quo was that iron ore, which also froze and became unworkable, was left in place to thaw in spring, meaning the fact it couldn’t be shipped in winter was irrelevant. But for any commodity that is not iron ore in 1950s conditions, a shipping route closed for months out of every year can’t be integrated into a just-in-time supply chain.

Great article. There are a few other factors to consider that I can think of, where AVs and Alto are concerned:

—Will AV trucks take freight share from rail, thus potentially freeing up rail lines for faster passenger service that could be a cheaper alternative to ALTO?

—Will AVs help solve the first-mile last mile problem, thus making people more likely to ride ALTO..or alternatively, more likely to fly instead of taking ALTO?

— Will AVs push up the price of fuel, or perhaps push down the price of fuel, which could in turn push up or down demand for ALTO?

…there’s a lot to consider. It’s hard to predict, though I share the concerns you raised in this article.

AV also wins on time if the train departures are infrequent. But travellers may prefer the train because it is smooth enough to get the laptops out. Time in an AV will be noisy and jittery.